Text size

Line height

Text spacing

VAT - Value added tax, is levied at the standard rate of 15% on the supply of goods and services by registered vendors. The tax rate was 14% until 31 March 2018.

What is VAT?

Value-added Tax is commonly known as VAT. VAT is an indirect tax on the consumption of goods and services in the economy. Vat is charged at each stage of the production and distribution process and it is proportional to the price charged for goods and services.

A person who is obliged to register for VAT is referred to as a vendor.

Who should register for VAT?

A person carries on an enterprise in the Republic (or partly in the Republic), it is obliged to register as a vendor.

"A vendor making taxable supplies of more that R1 million per annum must register for VAT. A vendor making taxable supplies of more R 50 000 but not more than R1 million per annum may apply for voluntary registration. Certain supplies are subject to a zero rate or are exempt from VAT. It is mandatory for a person to register for VAT if the taxable supplies made or to be made is, in excess of R1 million in any consecutive twelve month period. "

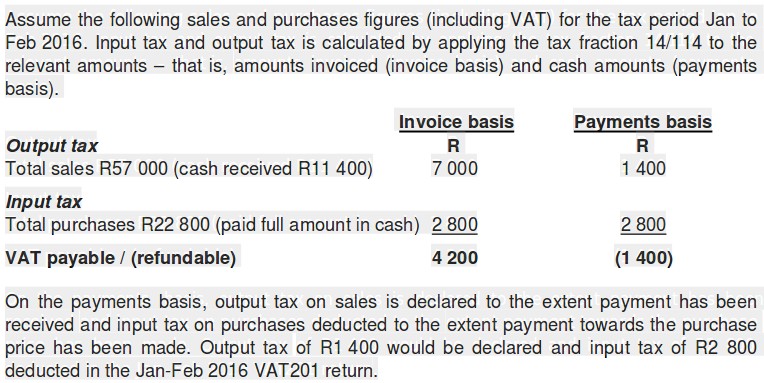

Example between Invoice and Payment basis VAT according to VAT404 SARS:

Output Tax and Input Tax

Output Tax is the Value added tax on Sales, if the Practice or Company are registered for VAT at SARS. Output Tax must be calculated on all the Sales or service that the Practice or Company sell or supply.

Input Tax is the Value added tax on Expenditure if the Practice or Company are registered for VAT at SARS. Input Tax will be added on the slip or Invoice you have paid for service rendered for the company or practice or goods your company or practice have bought. The supplier or company must be registered for VAT otherwise you will not be able to declare the VAT on the purchase.

Output Tax must be paid to SARS and Input tax your company can claim back. You will complete a VAT201 form on SARS eFilling. The Input Tax will be deducted from the Output Tax and the company or practice will pay the difference or claim back the difference.

When to apply 14% or 15% VAT Rate {www.golegal.co.za/vat-rate-increase}

"It follows that unless one of the special time of supply rules apply to the relevant supply, VAT at 15% will need to be accounted for on any supplies in respect of which an “invoice†is “issued†by the vendor on or after 1 April 2018, or any payment relating to that supply is received by the vendor on or after that date. Where an invoice is issued or any payment is made in relation to a supply before 1 April 2018, the relevant supply will be deemed to have been made and VAT at 14% will apply. Specific time of supply rules apply to, inter alia, supplies between connected persons (such as a group of companies), credit agreements subject to the National Credit Act, rental agreements, construction-related supplies of goods or services, the progressive or periodic supply of goods, instalment credit agreements, fringe benefits and leasehold improvements.

Importantly however, the VAT Act also provides for the position where goods are to be provided, or services performed, before the date that an increase in VAT becomes effective (1 April 2018) but such goods or services are deemed in terms of section 9 to have taken place after the date the VAT rate was increased. Section 67A of the VAT Act in essence provides that in these circumstances, the “old†rate of 14% will continue to apply to the goods provided, or services performed, prior to 1 April 2018, notwithstanding that those supplies are in terms of section 9 deemed to take place after 1 April 2018. Section 67A requires a “fair and reasonable apportionment†of the consideration for the supply that straddles the increase date. This rule applies specifically to rental agreements, periodic or progressive supplies, and construction-related supplies of goods and services. Section 67A further provides specific rules in relation to the sale of fixed property or the construction of any new dwelling. Where the price in respect of the fixed property, dwelling or construction in question was determined or stated in a written agreement in force before the date the VAT rate was increased, and the supply thereof is deemed in terms of section 9 to take place on or after the date upon which the VAT rate was increased, the VAT rate to be applied to such supplies is the “rate at which tax would have been levied had the supply taken place on the date the agreement was concludedâ€. Finally, section 67A also provides that in the case of a lay-by agreement, any deposit paid before the VAT rate was increased that is applied as consideration for a supply of goods or services after the VAT rate was increased, must be taxed at the rate that applied at “the time the agreement was concludedâ€.

Taxpayers need to ascertain when their supplies are deemed to have taken place under section 9 of the VAT Act, consider whether any of the special rules provided for in section 67A apply, and ensure that their systems are geared to identify those supplies that will be deemed to have taken place after 1 April 2018."

Existing agreements/pricing arrangements

The VAT that a vendor is required to account for on its supplies (output tax) is only recoverable from the recipients of those supplies if there is a contractual right to recover such VAT. There is no general legislative right of recovery, except where there is a change in the rate of VAT. Section 67 of the VAT Act provides that where the rate of VAT is increased (or decreased) in respect of a supply of goods or services in relation to which “any agreement is entered into by the acceptance of an offer made before the tax was increasedâ€, the vendor may recover such additional tax “as an addition to the amount payable by the recipient to the vendorâ€. The vendor may not, however, rely on the provisions of section 67 if there is a written agreement to the contrary, that is, the written agreement specifically provides that the vendor may not recover any increase in the VAT rate.

Bad debts

A vendor is able to claim VAT relief where a debt relating to a taxable supply in respect of which the vendor has accounted for output tax is treated as “irrecoverableâ€. The vendor may have now accounted for VAT at 14% in respect of a supply that was made before 1 April 2018 but the consideration for the supply is now regarded as “irrecoverableâ€. What rate of tax should be applied? In terms of section 22(1) of the VAT Act the vendor may only claim relief based on the VAT rate that applied to that particular supply. Taxpayers will need to ensure they are able to identify the rate of tax that must be applied in determining the relief available under section 22, where an amount of consideration is treated as “irrecoverableâ€.