Best Practice Guidelines: Healthcare Management Internal Controls

Best Practice Guidelines: Healthcare Management Internal Controls

Copyright © 2020 GoodX Software. All rights reserved.

GoodX online Learning Centre

learning.goodx.co.za

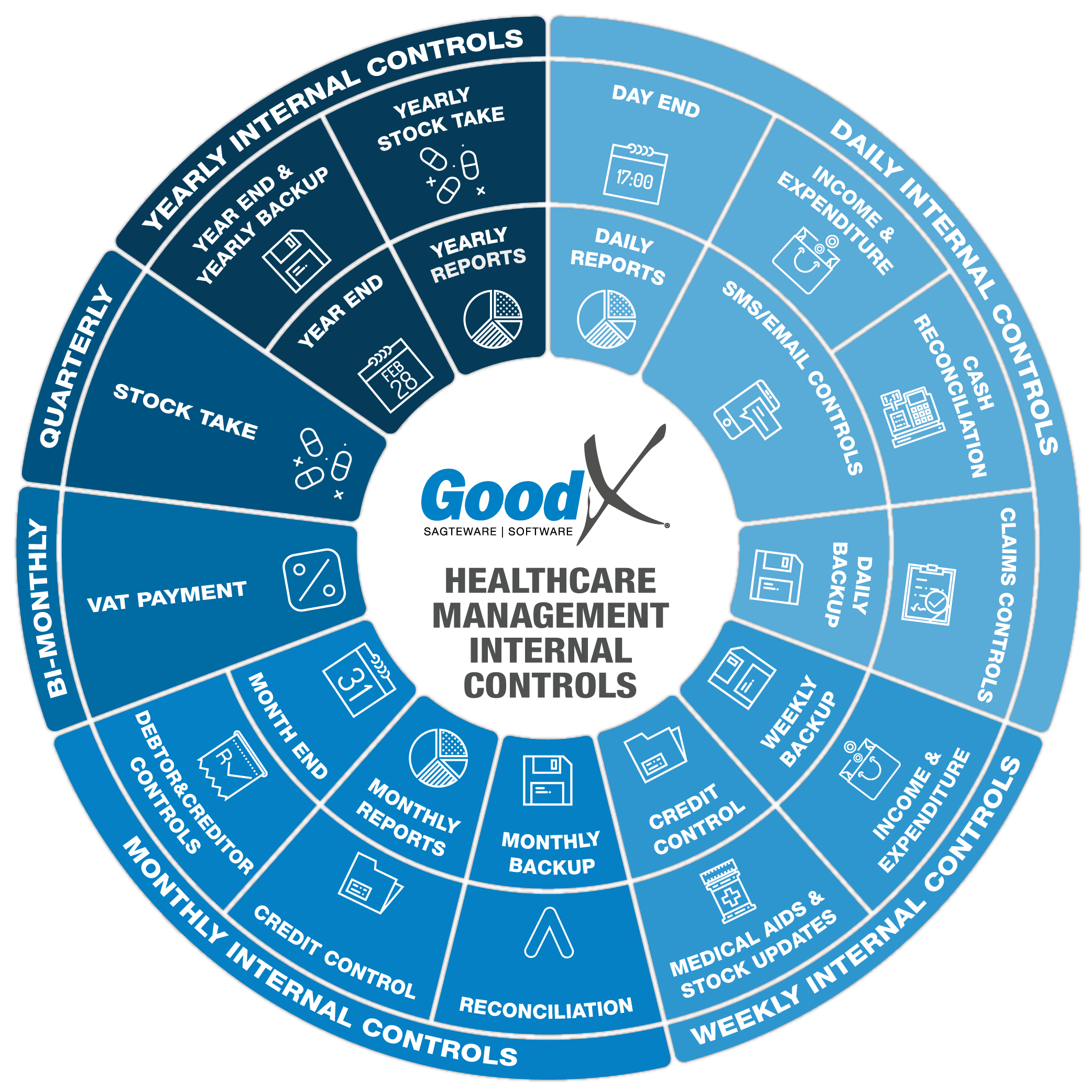

7. Yearly Internal Controls Summary

7.2. Yearly Stock Take

With each financial year the practice must do a full stock take on all items in the practice on the last day of the financial year. The stock take needs to be done after all transactions have been finalised for that financial year and need to be done on the last day of the financial year.

There must be an auditor on that day to do the necessary spot checks to validate the stock take and the financial manager must sign off the variance report. Please remember that between 5% to 10% variance on the total value of the stock on hand will be approved, depending on the auditors. When there is a variance of more than 5% - 10% the auditors will not sign off the audit report.

The auditors will take the final stock on hand report and choose a certain number of items, count the quantity on the shelf to check if it matches the quantity on paper and also a certain number of items to count the quantity on paper to check if it matches the quantity on the shelf. Ensure that the stock take is correct and reliable.

Stock Take procedures

Please refer to the Stock Management Guidelines book for the full information on the stock take procedures. In the internal controls the following will be important to check and the steps to be followed:

1. Finalising the Stock Take: Variance Report

1. Variance investigation

The system will calculate the difference between the counted quantity and the system quantity as per the snapshot. If you take your counted quantity and compare it to your system quantity you will have your variance.

Important pointers you have to look at on your variance:

- High-value items

- Items with a variance of more than 20, depending on your number of items in the practice

- Items with a variance of more than R 300 (currency value), depending on the value of the items in the practice

- Typing errors

- Items that were not counted

Spot Checks to ensure the accuracy of the quantity that was counted:

- Choose 10 items and count those items from the paper to the shelf.

- Choose 10 items from the shelf and count them back to the paper.

- Ensure the quantity is correct.

- When the quantity is not correct according to the spot checks the items need to be recounted.

- Take another sample of items and check the quantity and reliability. 10 other items must be used.

- When the items in the spot checks were incorrectly counted, the whole stocktake needs to be recounted.

If you pick up anything on your variance that was incorrect you must correct the mistake:

- If you Counted incorrectly or have made a typing mistake, you can still change your counted units and reprint the Variance report.

- If you have not Billed all your Patient files you must ADD the quantity to the stock count of that item on the counted units of the stock take.

- If you did not Capture a Credit Note on the Patient you must DEDUCT the quantity from your counted items on your stock take.

- If you did not capture all your Creditors or Supplier invoices you must DEDUCT the quantity from your counted items on your stock take.

- If you have not captured a Credit Note from your Supplier you must ADD the quantity to the stock count of that item on the counted units of the stock take

In Best practice, a Variance of 5% - 10% or less is acceptable on the value of your stock items. Anything more than 10% is a warning to start getting concerned and you must investigate immediately.

You must be able to explain to the auditors any and all variances in your Stock.

There is an option on the variances to only show the modified items, to assist in shortening the list and concentrating on the items with a variance.

2. Editing the quantity

When you have investigated all the variances you can still correct incorrect quantities. People make mistakes and a finger fault is really easy, or if you have counted incorrectly.

Remember that the quantities of your stock items on the report are all the counting locations in that warehouse added together.

3. Post Stock Take

When you have investigated all the variances on the items you must post your stock take for the system to adjust the items to the counted units.

The best practice is to post the stocktake within 24 hours after the stocktake.

The system will make a negative adjustment if the counted units were less than the quantity on the system and a positive adjustment if the counted units were more than the quantity on the system. This will be on the time and date stamp as of your snapshot.

You can also set up your stocktake to automatically do a re-evaluation of your stock value. This is a best practice because the purchase price increases and decreases a lot over time and varies from supplier to supplier. If you evaluate your stock with every stock take it will be at the best value.

The Final report will show the value and quantity that the system will have as the Stock on hand. Please remember that the quantity and value will differ if the practice started treating the patient again before the reports are printed.