Best Practice Guidelines: Healthcare Management Internal Controls

Best Practice Guidelines: Healthcare Management Internal Controls

Copyright © 2020 GoodX Software. All rights reserved.

GoodX online Learning Centre

learning.goodx.co.za

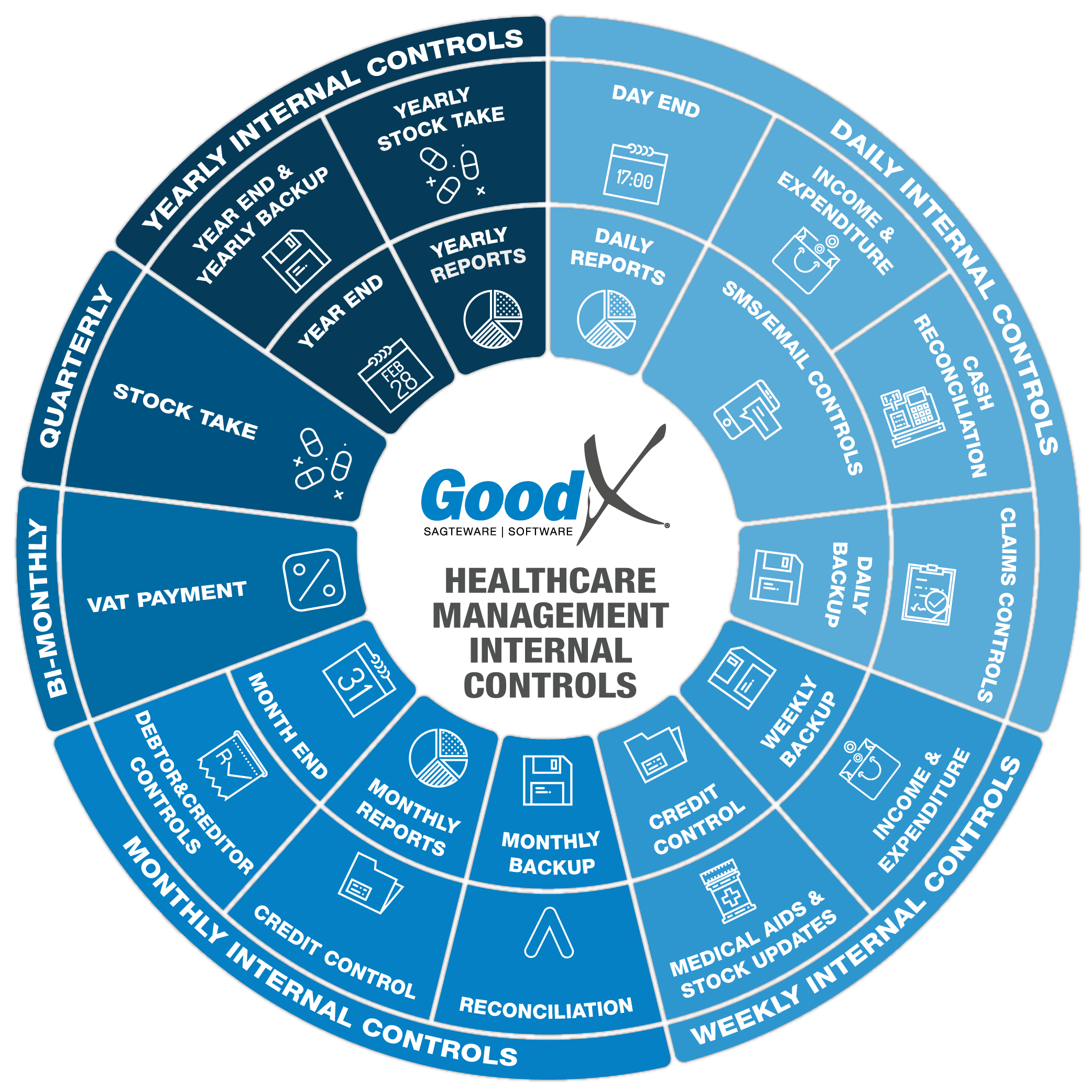

4. Monthly Internal Controls Summary

4.1. Debtor & Creditor Controls

The focus on the monthly debtor and creditor controls are the episode management, journals, interest and any other transactions that have not been finalised.

1. Invoices

Episode Management

Check at the end of each month if all episode numbers have been received from practitioners and that all were invoiced.

2. Journals

Journals are done for three main reasons:

- Bad debts written-off

- Small balances written-off

- Settlement discount.

These journals need to be finalised by the end of the month so that the age analysis report will be clear of amounts that should not reflect on the age.

Reports of all these journal transactions should be kept and only certain staff should have access to create journals.

3. Interest

Outstanding debtor accounts can be charged with interest depending on the contract with patients and the registration of the practice with the National Credit Council.

A certain percentage can be charged as Interest on outstanding amounts depending on the age that the amount is outstanding. Please make sure of all the regulations before doing this.

The charging of interest is done monthly to ensure that interest is charged on correct amounts by using the Debtors drill-down report and filtering on the interest tariff code.

4. Assistants

When the practice makes use of assistants, the assistant codes will be invoiced on the patient's account and receipts will be received from the medical aids or patients. The receipts need to be allocated to the patient accounts to ensure the correct reporting on the assistant creditor.

Assistants must get paid for their services. The Assistant Audit report will indicate which codes were billed and collected and which amounts are therefore due to the assistants.

Check the Assistant's Age Analysis report to ensure that all Assistants were paid. This will also be part of the Creditor checks.

1. Creditor and Supplier Controls

The following must be checked on a monthly basis:

- Check if statements that have been received from creditors at the end of the month, balance with the payment advice of GoodX for each creditor.

- Check if all invoices and credit notes/debit notes have been captured and received as per the Creditors' statements.

- Make sure all differences were investigated and resolved.

- Confirm that payments made to creditors were allocated to the correct invoices and that payments display on their statements.

- Ensure that unpaid invoices reconcile with the actual statements of creditors.

2. Assistants

All transactions on the debtors side must be up to date before the assistant audit report can be used successfully.

The assistants need to get paid for their services. The Assistant Audit report will indicate which codes were billed, and collected and what amounts are therefore due to the assistants.

Check the Assistant's Age Analysis report to ensure that all Assistants were paid. This will also be part of the Creditor checks.

Please double-check the payment arrangement with each assistant:

- Check immediately before the full payment is received.

- Check after the full payment was received.