Best Practice Guidelines: Healthcare Management Internal Controls

Best Practice Guidelines: Healthcare Management Internal Controls

Copyright © 2020 GoodX Software. All rights reserved.

GoodX online Learning Centre

learning.goodx.co.za

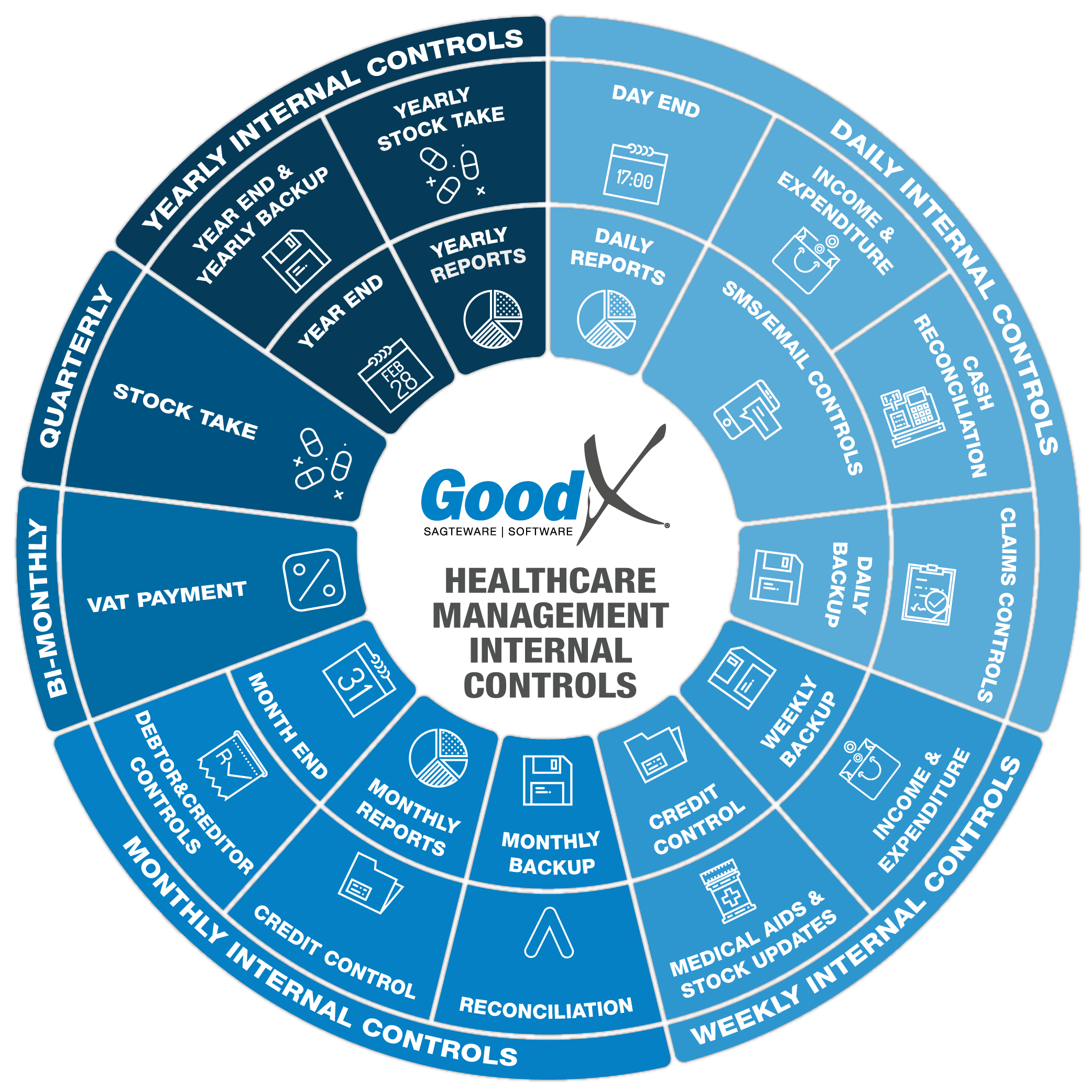

2. Daily Internal Controls Summary

2.3. Cash Reconciliation

Practices have cash in the cash register and cash in their petty cash bins. These two are not to be confused with one another, although some practices choose to utilise the cash register like a petty cash bin. Both the cash in the cash register and the cash in the petty cash bin must be accounted for.

The controls in this segment enable the practice manager to:

- Reconcile all the cash and credit card payments as received through the cash register to the daily cash register session as documented on the system.

- Reconcile all cash payments with the Deposits Report if the practice does not use the cash register (it is like a manual cash-up where the cash in the cash bin is matched with the physical cash receipts in the cash receipt book.

- Reconcile all the petty cash in the bin to the petty cash account etc.

1. Cash Register

The cash register is a function in GoodX that keeps a record of all cash and card payments. The cash in the physical cash bin must reconcile daily with the cash register records in GoodX and the card payments on the system must reconcile with the card machine's daily printout.

All cash received from patients can be used for small expenses in the practice BUT the money must first be transferred to the petty cash account.

The cash register has a float that must be set up correctly and reconciled daily.

When a receipt was processed with the cash register, any correction must also be done with the cash register so that the cash register will balance.

Process for the Cash Register

a. Session Report for Cash Register

- The report is used to view all transactions captured during the users' session.

- Check the session number, date and time it was started and by which user.

- Confirm the cash and credit card payment details and their totals.

- Check any discounts, write-offs or rounding values.

- Check any receipt reversals (corrections)

b. End Session for Cash Register

Every day the session must be finalised and a new session must be created for the new day's transactions.

- Check the session number, date and time it was started and by which user.

- Make sure all the card and cash receipts were captured before ending the session.

- Check any receipt reversals (corrections)

- End the session so that the reconciliation process can start.

c. Capture user cash-up for Cash Register

Capture the cash as you count the cash in the cash bin and also count the card payment slips together OR use the card payment total on the summary slip from the card machine.

- Check the session number, date and time it was started and by which user.

- Confirm the cash and credit card payment details and their totals.

- Check any receipt reversals (corrections)

- Capture the cash and the card totals.

- Post the cash-up.

d. Reconcile Session Report for Cash Register

This is used to reconcile the user's session with the actual counted cash and slips with what has been posted into the system

- Look at the "User Values" - this is what the user manually counted.

- Look at the "Difference" this should be the difference between what was posted to what was actually counted.

- Investigate the differences and correct where this can be corrected.

- Mark the reconciliation as completed if everything is balancing and the difference was explained.

2. Deposit report (Debtor Transaction Drilldown Report - Deposit Tab)

The Deposit report indicates all the receipts that were captured on the system grouped by the different type of payment method and all the Receipt corrections - Receipt written back.

The report can be used for fault finding and for reconciling the Cash, Card and EFT payments on a daily basis when the practice is not using the Cash register function.

The following information will be found on the report:

- Transaction and Capture Date.

- Deposit number.

- Detail of the receipt or correction.

- The user who posted the transaction.

- Total that was received or written back.

- Total per receipt type group together.

The report can be printed at the end of the day. The cash in the cash bin must be counted and reconciled back to the cash section minus the cash corrections, and minus the float in the cash bin.

The card payments total on the report minus the card corrections must reconcile with the card slip that was printed at the end of the day at the card machine.

3. Cashbook report

The Cash Book report shows all the receipts and receipt written back for a certain type of receipt that was done for a certain period. The report is drawn per cash book, for example:

- Cash/Card/Electronic/ERA's.

- Bank/Petty Cash/Home Loan.

The Cash Book report can be used for fault finding and to recon every day, week or month to the correct type of receipt that was done.

Petty Cash

Petty Cash is the cash in the petty cash bin OR a credit/debit card that is used to pay for expenses for the practice, e.g. milk and coffee or cleaning materials.

The cash received from patients can be transferred to the petty cash for general expenses OR money can be transferred from a bank account OR cash can be drawn from the bank.

The expenses must be captured in the accounting module in GoodX so that the petty cash account can be reconciled with the actual money in the bin/account.

All physical slips/invoices received for expenses must be kept for reconciling and auditing purposes.

Process for the Petty Cash

a. Transfer from Cash Register to Petty Cash

If cash that was received from patients is used for petty cash, the transfer must be done daily from the Cash register cash book to the Petty Cash cash book.

- Check the total cash you are taking out of the cash received from patients.

- Create a payment (cheque) in GoodX from the Cash register cash book to the Petty Cash cash book.

b. Income from a bank account

If the cash is received into the petty cash from a bank account, be it physically drawn or transferred:

- Make out a cheque from the bank account to the petty cash to indicate the cash received into the petty cash.

- The Petty Cash balance will increase.

c. Expenses paid by the petty cash

When cash is used from the petty cash to pay for expenses the expenses must be captured.

- Ensure you have a physical slip/invoice for every expense

- Make out a cheque from the petty cash to the correct expense ledger account in GoodX to indicate that there was an expense

- The balance will decrease when an expense is captured.

d. Reconcile the petty cash

At the end of every business day, the petty cash must be up to date with all transactions that were done during the day. The petty cash must be reconciled.

- The Petty Cash will have a balance from the previous day

- The income will be plus and the expenses will be minus

- The closing balance must balance with the petty cash in the cash bin

- Reconciliation will be done through the accounting module and Cash Book reconciliation.

Some practices use the cash register as a petty cash bin and link the cash register to a petty cash, cash book. However, if you have a separate petty cash bin, you need to make sure that all petty cash is counted and reconciled to the cash slips in the bin.