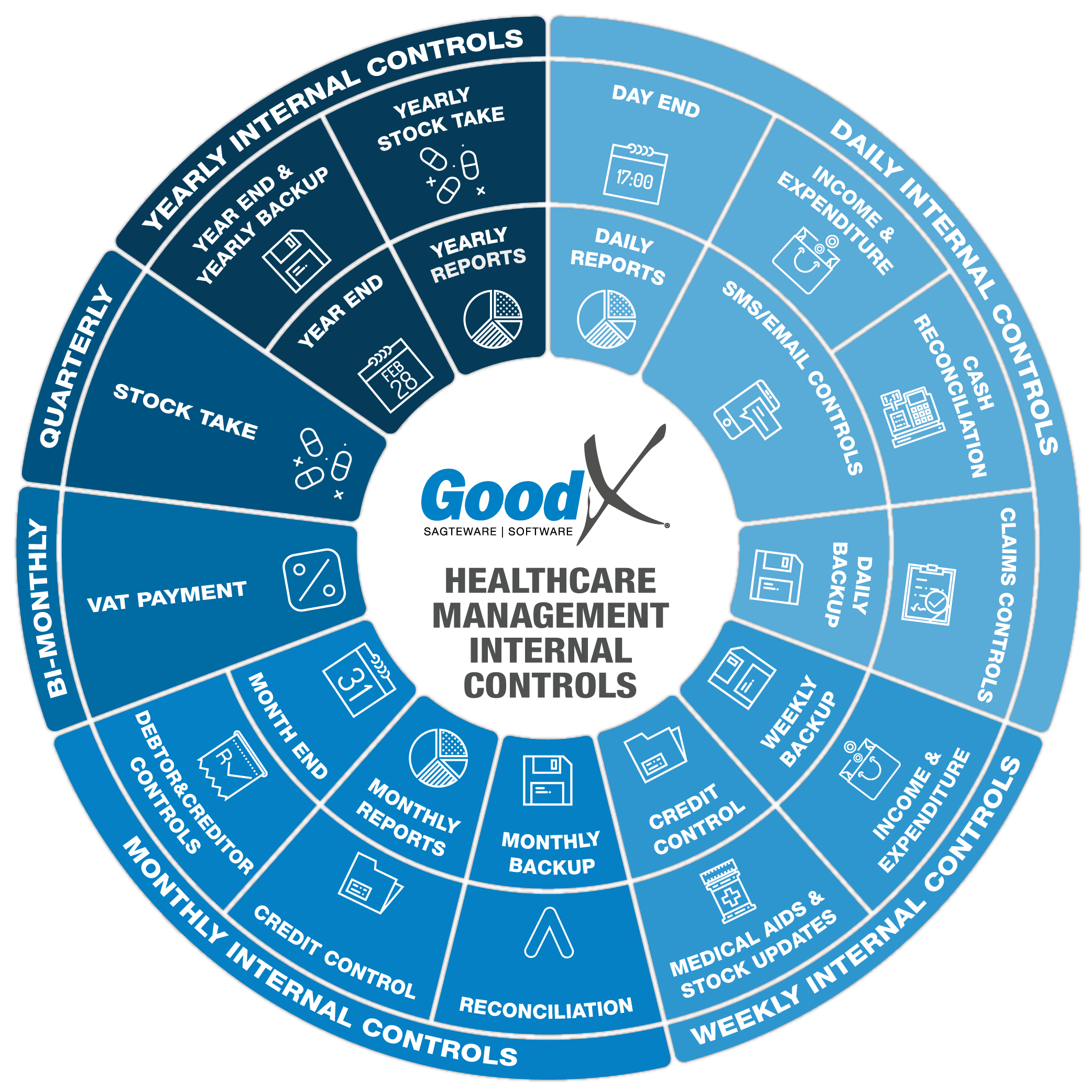

Best Practice Guidelines: Healthcare Management Internal Controls

Best Practice Guidelines: Healthcare Management Internal Controls

Copyright © 2020 GoodX Software. All rights reserved.

GoodX online Learning Centre

learning.goodx.co.za

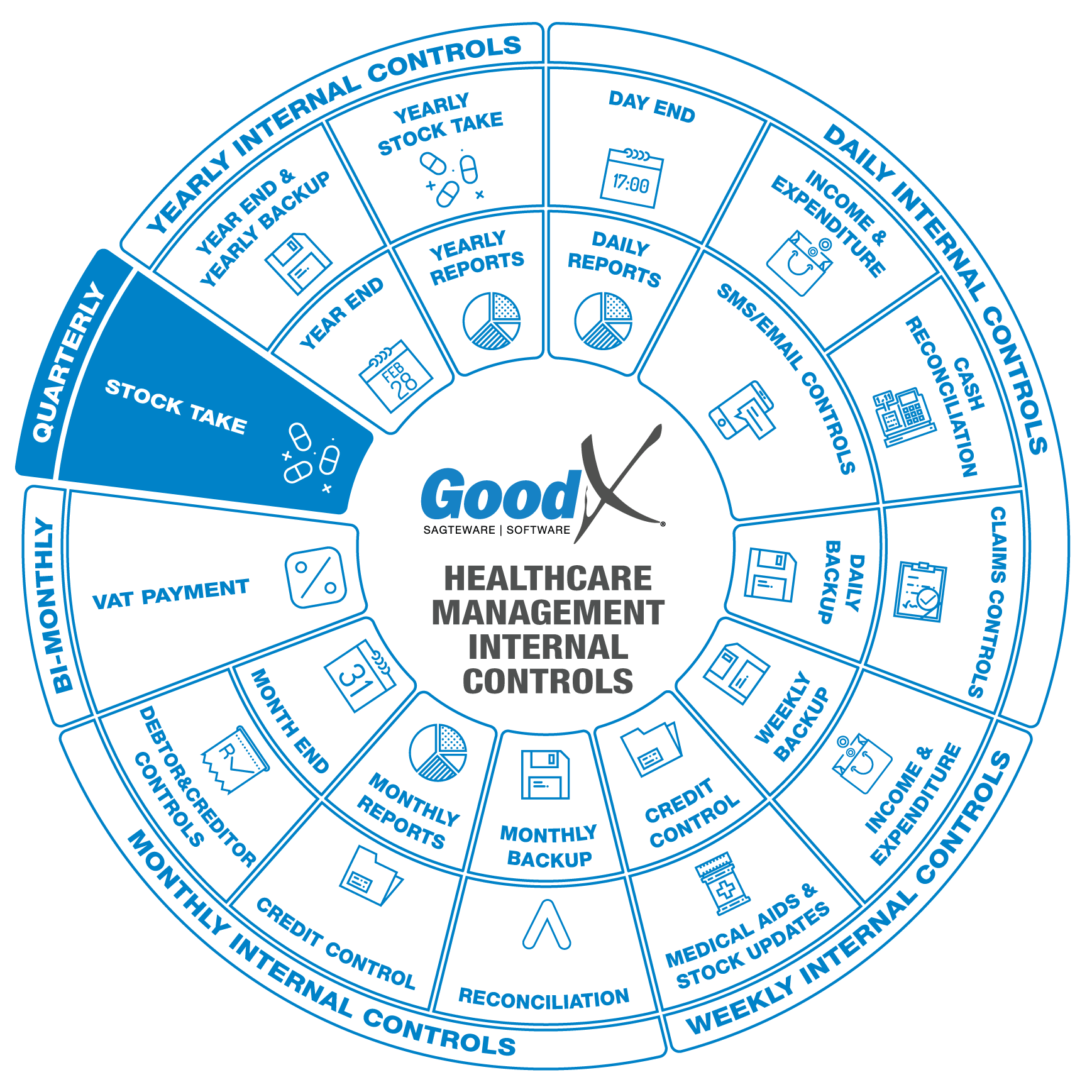

6. Quarterly Internal Control: Stock Take

Stock control is a daily task. The management of the stock items in the practice is important to prevent financial loss and possible legal action against the practice.

Schedule 5, 6 and 7 medicines must be documented by hand in a register immediately after those items have been used. Stock take must be done daily on these items.

Please refer to the Stock Management Guidelines for more detail on managing stock control on a daily basis.

Stock take must be done on Materials/Consumables and Medicine. If the practice is using cleaning materials and stationery, stock take can also be done on these items.

Stock Take Procedures

There are a lot of rules applicable to medical stock items depending on the Schedule of the item. Please make sure your knowledge is up to date with all the latest regulations.

Some important information to remember with stock takes:

- Schedule 5, 6 and 7 medication must be counted every day and a handwritten register must be kept on this medication.

- The best practice is to do a full stock take every three months (quarterly).

- There must be a full stock take with the practice's financial year-end.

- You must have an external auditor on-site with the financial year-end stock take to audit the quantities you counted and have the auditor sign off if the count was correct.

- Stock counts must be done in pairs of two people.

- Each stock count sheet form must have two signatures and the date the count was done on.

- Original stock counts are not allowed to be captured on excel or any other electronic software, where the count can be adjusted afterwards. This prevents fraud.

- There must be a hard copy of the counted items on a stock sheet that is written in pen.

- Keep a copy of your captured stock count on your system.

- Keep a copy of your variances on your counted quantities and the quantities on the system you are using.

- Please refer to the Stock Take process for more important information

Stock takes are important for the following reasons:

- To comply with laws and regulations.

- To avoid financial loss on stock inventory.

- To uncover theft.

- To manage stock levels.

- To manage the best interest of your practice.

The following steps will be followed during a stock take:

1. Inform all employees 2 weeks in advance of when the stock take will take place.

2. Get all the information up to date and prepare for the stock take.

3. Print counting sheets, update and reprint.

4. Check the unlinked item report.

5. Create a snapshot.

6. Count the stock items and the quantity of each item.

7. Capture the stock quantity that was counted, into GoodX.

8. Consolidate all the counting locations into one General bin per warehouse.

9. Print the Variance report.

10. Edit and correct quantities that were counted incorrectly.

11. Post the stock take.

Take note: All the steps must be performed on all warehouses if multi-warehouses are used.

Reporting on stock take

Reports will be used for management purposes and financial decision-making.

1. Variance Report

The system will calculate the differences between the counted quantities and system quantities as per the snapshot. If you take your counted quantities and compare it to your system quantities you will have your variance.

Important information to consider when reviewing your variances:

- High-value items

- Items with a variance of more than 20 items, depending on your number of items in the practice.

- Items with a variance of more than R300 currency value, depending on the value of the items in the practice.

- Typing errors.

- Items that were not counted.

All errors must be corrected immediately:

- If you counted incorrectly or made a typing mistake, you can still change your counted units and reprint the Variance report.

- If you have not Billed all your Patient files you must ADD the quantity to the stock count of that item on the counted units of the stock take.

- If you did not Capture a Credit Note on the Patient you must DEDUCT the quantity from your counted items on your stock take.

- If you did not capture all your Creditor or Supplier invoices you must DEDUCT the quantity from your counted items on your stock take.

- If you have not captured a Credit Note from your Supplier you must ADD the quantity to the stock count of that item on the counted units of the stock take.

Best practice dictates that a variance of 5% - 10% or less is acceptable on the value of your stock items. Anything more than 10% is a warning sign and you should investigate the variance immediately.

There should be proper explanations for all variances in your stock to be provided to the auditors.

2. Final report

The Final report reflects the stock on hand after the stock take has been posted. This is the quantity and value of all the items that were included in the stock take. This is also the quantity that must be in the practice after the stock take if the stock take was done correctly and no movement happened after the snapshot was done and the finalising of the stock take.