Best Practice Guidelines: Healthcare Management Internal Controls

Best Practice Guidelines: Healthcare Management Internal Controls

Copyright © 2020 GoodX Software. All rights reserved.

GoodX online Learning Centre

learning.goodx.co.za

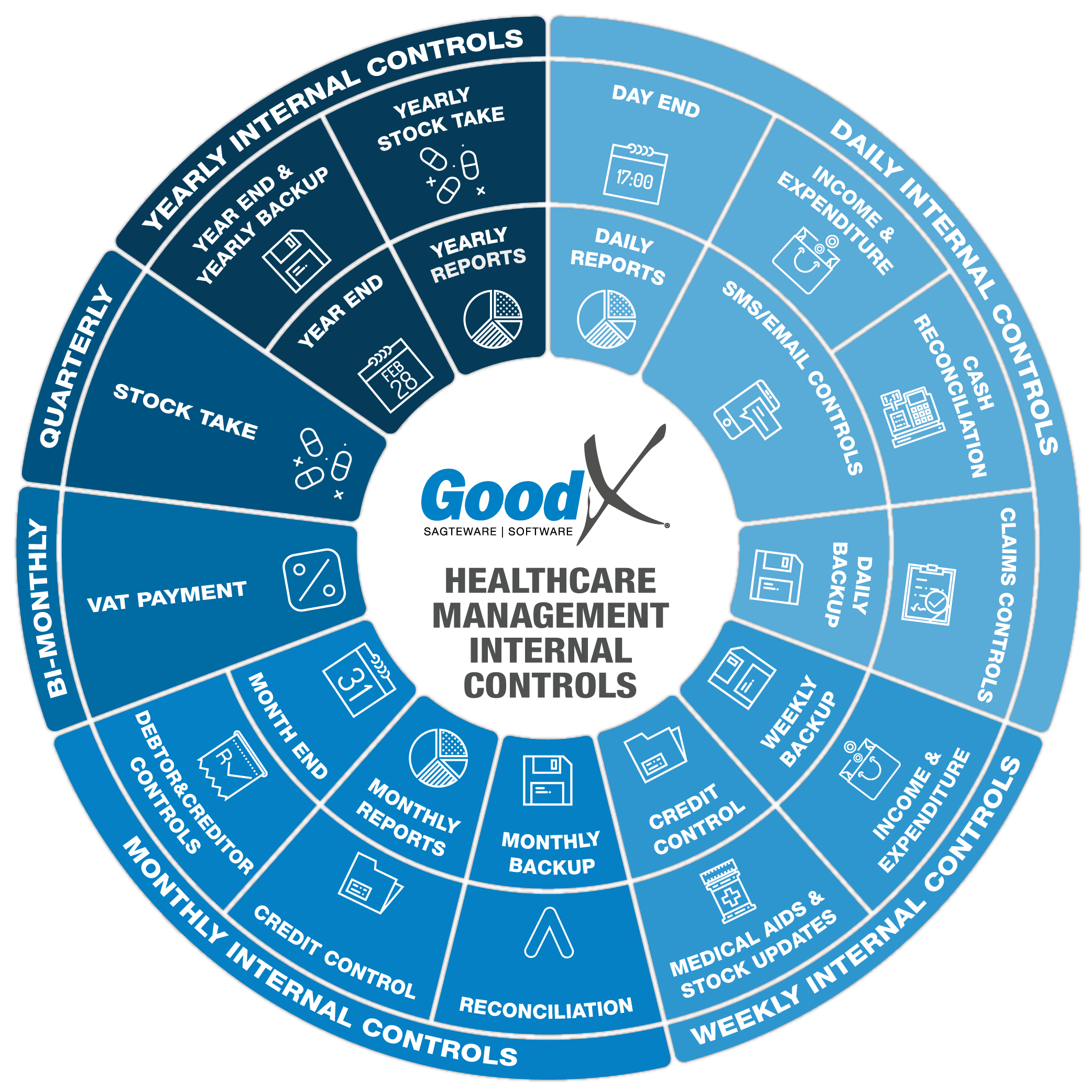

4. Monthly Internal Controls Summary

4.3. Reconciliation

Reconciliation is an accounting process that uses two sets of records to ensure figures are correct and in agreement. It confirms whether the money leaving an account matches the amount that's been spent, and ensures the two are balanced at the end of the recording period. Reconciliation provides consistency and accuracy in financial accounts.

Reconciliation is particularly useful for explaining the difference between two financial records or account balances. Some differences may be acceptable due to the timing of payments and deposits. Unexplained or mysterious discrepancies may be signs of error or theft.

The reconciliation process is also used to make sure that the stock you captured on your software is in agreement with the stock you have on hand in your practice.

Reconciliation thus compares all transactions and items captured on your software with what is physically happening in the practice - the software system must reflect reality.

Examples:

- All card slips must be reconned with the card summary slip produced by the card machine at the end of the day, which in turn must be reconned with the card cashbook account, which must recon with the card deposits on your bank statements;

- All stock items in your practice must reconcile with the closing balance of your stock items as per your software system;

- All items on your bank statements must reconcile with the transactions in your bank cash book.

The process of reconciliation will assist the practice to check that all transactions and items were correctly captured and allocated.

A reconciliation report will show the following:

- Opening Balance - O/B is the closing balance of the previous financial period.

- Transactions - All transactions (Deposits, Payments and corrections) for the current financial period.

- Closing Balance - C/B is the opening balance plus or minus all the transactions that took place in the current period - this will give the closing balance for the current financial period and is used for the opening balance of the next financial period.

Reconciliations to be done:

- Debtor and Creditor transaction drill-down report must reconcile with the Age Analysis for the Debtors and Creditors.

- Main Cashbooks (Bank Accounts, Credit Cards, Home and Car Loans, Petty Cash and any other accounts that you receive statements every month for)

- Auxiliary cashbooks (Cash, Card, Electronic and ERA cashbooks)

- Stock (Variance report, Stock on hand)

- Trial balance - check if the totals of the debit and credit columns are the same.

Debtors Transaction drill down (Movement summary)

The movement summary will be drawn from the Debtor transaction drill down report (Daybook). The movement summary is applicable to Debtors. The Movement summary is a tab in the drill down report.

The Movement summary is divided into the Opening Balance, Turnover, Cashflow, Journals and Closing Balance which must balance with the Debtors Age Analysis for the same period. The Movement summary will display a check mark if the data is balancing. When the data is not balancing, please contact GoodX to investigate the error.

1. Creditors Transaction drill down (Ledger tab)

The Ledger tab in the Creditor transaction drill down report is applicable to Creditors. The Ledger Tab is divided into the Opening Balance, Creditors Invoices, Credit Notes, Payments and Closing balance which must balance with the Creditors Age Analysis for the same period.

2. Creditors Statements:

All Creditor statements need to be reconciled back to the payment advice in the system.

- Check the opening balance of the current month's comparison with the closing balance of the previous month.

- Check all invoices on the statement as opposed to the invoices on the system

- Check all the payments on the statement as opposed to the cheques on the system.

- Check all credit notes have been allocated on the statement and on the system.

- Check the closing balance on the statement as opposed to the closing balance on the system for the current month.

Stock control is an important part of any practice that uses medicines OR consumables/materials.

1. Variance report

The Variance report must be generated during a stock take and must be reconciled and all differences investigated. The Variance report will show all the differences in the actual stock against the stock captured on the system.

2. Stock on Hand

Stock on Hand can be reconciled by checking the Stock on Hand report and counting some of the expensive items to see if it is balancing. This is also called Cycle counts under the Stock Take section in the booklet.

1. Main Cashbooks

The main cashbooks always have an opening balance and a closing balance for each period or specified dates.

Workflow for Main Cashbooks with a Bank statement

- The bank statements must be imported into the main cash books.

- The expenses will be shown as cheques and the income will be displayed as deposits.

- All transactions must be allocated to the relevant Ledger Accounts or other Main Cash books.

- After all the transactions have been allocated and posted for the financial period, the recon must be done.

- The recon function will assist in reconciling the bank accounts and showing if all transactions were posted and allocated, by taking the difference between the opening balance and the closing balance and comparing these amounts to the transactions that were posted into the cashbook.

- Take the bank statement for the period that must be reconciled and check off all the transactions that are on the bank statement.

- When the cashbook balances, the top right balance indicator will turn green.

- The recon statement can be printed for record keeping.

- The recon will not post if there are differences.

Please Note: If the cashbook and the physical bank statement do not balance, there is probably some technical error:

- The date format should be YYYY/MM/DD but was imported as DD/MM/YY.

- Debit amounts that were imported as Credit amounts or the other way around.

- Incorrect Columns are indicated on the template.

- Lines on the imported bank statements that are missing between two different imports, eg if the bank statements are imported daily and there were transactions between 17:00 and 08:00 and the next day you only import from 08:00, the transactions between 17:00 and 08:00 will be missing in the cashbook.

Workflow for Petty Cash Cashbooks

- Normally petty cash works with cash and/or a bank account with a debit card.

- There will always be an opening balance - this will include the float in the petty cash bin.

- The expenses must be allocated to an Expense Ledger account.

- The income that is normally the amount that is used to replenish the petty cash bin again when the petty cash is depleted.

- In some cases, the income can also be from cash payments made by patients for services that the practice utilises for petty cash. Please also read the Cash reconciliation under Daily controls.

- The petty cash closing balance must be the same as the cash in the cash bin or the balance of the petty cash bank account.

2. Auxiliary Cashbooks

Auxiliary cashbooks are support cashbooks that assist in reconciling certain transactions in the Main cashbook. The Auxiliary Cashbooks must always calculate to ZERO when reconciled for a certain period. The opening balance and closing balance should therefore always be zero, meaning that the movement of all transactions must calculate to zero as well.

a. Cash Cashbook

When receiving cash payments from debtors, the cash will be allocated to the debtors account and also to a Cash Cashbook. The cash should be paid into a bank account on a daily, weekly or monthly basis, depending on the needs of the practice.

The payment into the bank account will be equal to the total amount of all the cash that was received from all the debtors for a certain period. This must balance with the Cash Cashbook and will be allocated to the Cash Cashbook from the Main cashbook (Bank Account).

The Auxiliary Cash Cashbook must always calculate to ZERO when reconciled for a certain period. The transactions that still create a balance indicates that the cash was not yet banked into the bank account.

Workflow for the Cash cashbook

- Depending on the workflow of the practice, cash will be counted daily and deposited into the bank account of the practice.

- Keep a list of all the debtors from whom the cash was received by generating the Cashbook report**. NB Make sure that all cash transactions on the report balances with your deposit slip to assist you later with the recon.

- All the debtor receipts are deposits in the recon function of the cash cashbook and the cash deposits in the bank account will display as cheques in the cash cashbook. (They display as deposits in the main cashbook and as soon as they are linked to the cash cashbook (auxiliary cashbook, they are cheques.)

- Multiple deposits in the cash cashbook (**all those listed on the Cashbook report that matches one deposit) must be checked to balance with the single cheque amount reflecting the deposit in the bank account. If your deposit slip and Cashbook report balanced as stated above, the matching will be easy.

- The system will show that the movement is balanced by showing green on the right hand side when all the correct deposits are checked to match the corresponding cheques. The movement should be calculated to ZERO.

- All cash received from the debtors that have been allocated to the Debtors account but have not been banked will show as unreconciled, and will only be reconcilable in the next period if the cash is banked on the 1st day of the next month/period.

- The unreconciled amount must balance with the cash in the practice or the cash slips received from the bank if it was deposited in the next period.

- The recon can be posted when all the transactions are balancing and the transactions that are only going to be banked in the next period are still unreconciled. All unreconciled transactions will be taken over to the next period for reconciliation.

b. Card Cashbook

When working with card payments from Debtors, the card payments will be allocated to the debtors account and also to a Card Cashbook. All the card payments that were received for the day will be added together and paid into the practice bank account from the card machine bank account.

The payment into the bank account will be a total amount of the card payments that went through the machine for that day. The Card machine will print a slip that will show all the card payments that were received from debtors for that day and the total of the Card payments. The total will show on the bank statement the next day. This must balance back to the Card Cashbook and will be allocated to the Card Cashbook from the Main cashbook (Bank Account).

The Auxiliary Card Cashbook must always calculate to ZERO when reconciled for a certain period. the transactions that are still left mean that this was not yet banked into the bank account from the Card machine.

Workflow for the Card cashbook

- The Card payments that went through the Card Machine must be allocated to the Debtors Account.

- Keep a list of all the debtors from whom card payments were received by generating the Cashbook report***. NB Make sure that all card transactions on the report balance with your summary slip to assist you later with the recon.

- The Card Machine will print a summary slip at the end of the day with all the card payments that went through the card machine for that day with a total that will be paid into the bank account of the practice. Normally the credit card and the debit card will be split into two different payments on the bank statement.

- All the different debtor receipts will be shown as a Deposit in the recon function and the Card payments into the bank account will display as Cheques.

- Multiple deposits in the card cashbook (**all those listed on the Cashbook report that matches one deposit) must be checked to balance with the single cheque amount reflecting the deposit in the bank account. If your summary slip and Cashbook report are balanced as stated above, the matching will be easy.

- The system will show that the movement is balanced by showing green on the right-hand side when all the correct deposits are checked to match the corresponding cheques. The movement should be calculated to ZERO.

- All card payments received from debtors that have been allocated to the Debtors accounts but have not been banked will show as unreconciled, and will only be reconcilable in the next period if the cash is banked on the 1st day of the next month/period.

- The unreconciled amount must balance with the card slips in the practice.

- The recon can be posted when all the transactions are balancing and the transactions that are only going to be banked in the next period are still unreconciled. All unreconciled transactions will be taken over to the next period for reconciliation.

c. Electronic Cashbook

When receiving EFT payments from debtors, the EFT payment will be allocated to the Debtors account from the Electronic Cashbook that was allocated from the bank account cashbook. The EFT payment will be paid into the bank account cashbook and will be allocated with the import of the bank statements. Then allocated to the Electronic cashbook and form the electronic cashbook allocated to the Debtors account.

EFT payments will always be an out and an in, in the Electronic cashbook. Always one Deposit and one Cheque.

The Auxiliary Electronic Cashbook must always end up to ZERO when reconciled for a certain period. the transactions that are still left mean that this was not yet allocated to the Debtors account allocated to the electronic cashbook from the bank account cashbook.

Workflow for the Card cashbook

- The EFT payments that were paid into the bank account must be allocated to the Electronic Cashbook.

- EFT payments that were allocated to the electronic cashbook must be allocated to the Debtors account.

- Keep a list of all the different Debtors for whom the EFT payments were received, by using the Cashbook report.

- All the different Debtors receipts will be shown as a Deposit in the recon function and the EFT payments into the bank account will display as a Cheque.

- There will normally be only one Deposit for each Cheque with the same amount, one a minus and one a plus.

- The system will show that the movement is balanced by showing green on the right-hand side when all the correct deposits are checked to the corresponding cheques and the movement calculates to ZERO.

- The EFT payments that were not yet allocated to the Debtors account will still be in the electronic payments as Cheques and not marked off against a Deposit. This must be corrected by making an EFT payment to the Debtors account.

- The recon can be posted off when all the transaction is balanced out.

d. ERA (Electronic remittance advice) Cashbook

When receiving ERAs from Medical aids, the EFT payment from the Medical aid will be allocated to the bank account and also from the ERA function to the ERA cashbook. All the claims on behalf of debtors that were approved from a specific medical aid will be added together for a certain period, combined into an ERA, and will be paid into the practice bank account.

The payment into the bank account will be the total amount of the different claims that were approved by the Medical aid for a certain period. The medical aid will combine all the debtor's approved claims for a certain period into one ERA and pay the amount into the practice bank account. The total will show on the bank statement. The amount will be allocated from the bank account cashbook to the ERA cashbook as a Cheque. An ERA will be imported into the software with the ERA function and when the ERA is posted from the ERA function, the total amount will be posted to the ERA cashbook as a Deposit.

The Auxiliary ERA Cashbook must always end in ZERO when reconciled for a certain period. Unreconciled transactions indicate that the ERA amount has not yet been paid into the bank account.

Workflow for the ERA cashbook

- All ERA payments in the bank account will have an ERA that needs to be imported through the ERA function.

- Keep a list of all ERAs that were imported to the debtors accounts, by using the Cashbook report.

- All the different debtor receipts will be shown as a Deposit in the recon function and the ERA amounts paid from the medical aids into the bank account will display as Cheques.

- There will normally be only one Deposit for each Cheque with the same amount, one a minus and one a plus.

- The system will show that the movement is balanced by showing green on the right-hand side when all the correct deposits are checked to the corresponding cheque and the movement calculates to ZERO.

- ERAs that were received from the Medical aids should not be posted before the payments were made into the practice bank account.

- The recon can be posted when all the transactions are balanced out.

e. Corrections

If there is a transaction on the cashbook that was posted incorrectly, the transaction must first be corrected before the recon can be done and finalised. All incorrect transactions must be corrected in the original place where they took place.

For example, if the receipt (Deposit) was allocated as a Cash payment but was a Card payment, a receipt written back must be done on the Debtors account and the receipt must be posted to the correct cashbook.

For example, if the amount that was imported from the bank statement was allocated incorrectly, the correction must be done through a financial correction in the correct bank account cashbook.

f. Trial Balance

To check if the Trial Balance report balances, check whether the total of the credit and debit columns match.